An Interchange Primer

It’s imperative for credit unions to understand interchange – the biggest component of non-interest income.

One of the most misunderstood, and possibly the most misaligned topic in the credit and debit card world is interchange. At a summary, it is a fee paid by a merchant, paid to the issuer, each time a credit or debit cardholder uses a card, in a store or online. The fee covers the cost of processing the credit or debit card; for a credit transaction the fee reimburses the issuer for the interest on carrying the balance during the cardholder’s debt repayment grace period; and the fee is intended to address the cost for zero fraud liability, which reimburses the cardholder in case of fraud. In addition, higher interchange is charged for signature rewards credit cards, to cover the cost of additional cardholder benefits such as cash back or auto rental collision damage waiver. The practice of a merchant paying the issuer interchange was established in 1971, when Bank Americard set 1.95% as the standard rate as compensation for the risk of card-issuing banks. Interchange is also paid to the ATM owner each time a cardholder gets cash out. Seems simple enough, but there’s much more complexity to it.

To understand interchange, its first necessary to get to know the “players” in the space. The merchant has an account with a bank, called the acquiring bank. The card holder was issued her card from an issuing bank. So there are two banks involved. Since there are thousands of merchant acquiring banks around the world, and even more issuing banks, the many to many relationships is simplified by having a card “brand” in the middle. The most common “brands” in the U.S. are Visa, MasterCard, American Express, Discover, and they form the networks that connects all the acquiring banks with all the issuing banks. Interchange “flows” through the network, from acquirers to issuers, and can be reversed in case of credits (for example when the cardholder returns an item) and for chargebacks (for example, fraudulent charges). Thus, interchange is bi-directional. Also, there is not just one interchange rate; there are literally thousands of rates. Each network brand sets their own rates based on market forces, and rates vary by merchant, card types, purchase volumes, and several other factors. What the merchant pays for is the ability to accept cards which includes interchange. The total of these fees is called the Merchant Discount Rate which is negotiated between merchants and their acquirer.

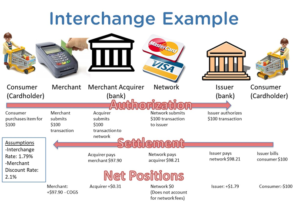

To better understand how interchange works, the next diagram shows the participants, and two flows: first the authorization of the purchase (left to right), then the settlement of the purchase (right to left). The consumer wants to make a $100 purchase from a merchant. The merchant requests authorization, which is routed through the network to that consumer’s issuing bank – to make sure they have funds in the debit account, or balance on their credit card, the card hasn’t been reported lost/stolen, many other factors are checked. Technically, the authorization, which happens in real-time, is processed on behalf of the merchant through a merchant processor, and is responded to by a credit or debit processor on behalf of the issuer. Note that the consumer on the left is the same person as the cardholder on the right.

In this example, assume the interchange rate for this particular transaction is 1.79%, and the merchant discount rate for this transaction is 2.1%.

Assuming the charge is authorized, the consumer’s debit account is deducted the $100, or a $100 charge is added to the credit card account, depending on the card type. The cardholder’s bank, the issuing bank, keeps the interchange, which in this case is $1.79, and settles the remainder, $98.21 with the merchant acquirer bank. The merchant acquirer, or more specifically, the merchant processor, charges the merchant a merchant discount rate. This rate includes a cost of processing the cards on behalf of the merchant, reporting, accounting, and also covers the interchange kept by the issuer. In this example, the merchant discount rate is 2.1%, ($2.10), of which $1.79, the actual interchange, went to the issuer, with $0.31 ($2.10 – $1.79) going to merchant acquirer/merchant processor.

In the end, the merchant receives $97.90: the purchase price minus the merchant discount rate, and their net is that minus the cost of goods sold. From this example, it becomes obvious that there are many moving parts to interchange, and many misunderstandings. Some common myths are:

Myth: Merchant pays the interchange rate. Fact: The merchants pay the Merchant Discount Rate (MDR) which does include interchange, plus charges from the acquirer/processor to cover costs of card acceptance and processing, plus ancillary services. MDR may be “blended” (e.g. one fee for all credit transactions, one fee for all debit transactions), a “mark-up” (e.g. interchange plus 0.20%), flat rate (e.g. $0.10 per authorization), monthly fee, or any hybrid.

Myth: Interchange keeps increasing. Fact: The Durbin amendment capped debit interchange for non-exempt FIs to 0.05% plus $0.21 plus $0.01 for fraud. Credit interchange has continuously been revised downward due to market forces and to encourage card acceptance.

Myth: Visa/MasterCard gets a “piece” of the interchange. Fact: Interchange is owed to the issuer, and is paid from the merchant acquirer’s funds. The networks do not participate in interchange. The networks impose negotiated network charges to the banks on both sides of the transaction, outside of the interchange process.

Myth: Interchange rates are secret. Fact: Rates are typically revised annually and published on the web. (Visa’s 2017 published rates here, MasterCard’s rates here). The brands have in limited instances negotiated specific rates with very large merchants, bringing down average interchange income to issuers. These negotiated rates with individual merchants are not made public.

As opposed to the simple example above, in real life almost all interchange rates are expressed as a percentage of the transaction plus a flat amount. Interchange rates vary greatly based on several factors. Looking at Visa’s published rates, interchange for buying gas with a debit card, paying at the pump is 0.80% + $0.15, capped at $0.95 total. Booking online for a hotel room or a car rental using a debit card is 1.70% + $0.15 (with no cap).

Interchange for credit cards have more variables: what kind of merchant, what kind of card, and how the card number is input. Supermarkets usually have the lowest interchange rates, since they have low fraud rates and are least likely to have chargebacks: 1.15% + $0.05 for a traditional rewards card, 1.65% + $0.10 for a signature credit card, and 2.10% + $0.10 for an elite card at a large volume supermarket. A card inserted into the chip reader at a typical retailer is 1.51% + $0.10, but if the clerk enters the card number manually, the interchange rate is higher, 1.80% + $0.10.

There are many other factors involved. Debit networks, such as NYCE, Star, Pulse, negotiate rates with individual merchants to accept debit cards at rates usually lower than what the “brands” networks charge for the same debit cards. The merchant (not the cardholder) has the option to route the transaction, and hence control the interchange rate paid, by choosing a debit network over a Visa or MasterCard network for debit cards. Commercial cards, typically corporate cards given to employees by companies to cover travel expenses, and fleet cards, have a separate set of rates, typically higher than traditional consumer cards. Merchants that have higher volume of chargebacks (whether from consumer disputes or from fraud) move into a higher interchange category, while the converse is also true. There is a separate schedule for large ticket items with smaller percentage and larger fixed amount. For example, online (card-not-present) Visa purchases made with a credit card over $25,000 have an interchange rate of 0.60% + $52.50. And on the other end of the spectrum, small ticket items, such as a cup of coffee, have their own rates, to encourage merchants to accept debit cards instead of cash: 1.55% + $0.04.

Interchange is the foundation of the credit and debit payment industry’s cost structure. For most issuers, it represents the single biggest component of non-interest income. It is also the source of funding for rewards programs. But interchange is complex and ever-changing, and budgeting both the income and the expense requires an in-depth understanding of the drivers, and how those drivers are changing over time. Let us know your thoughts and comments below.